The cost of ASRS reporting: what Australian companies spend (2026)

Read time: 9 minutes

The cost of ASRS reporting runs to roughly $1.3 million per entity to set up and around $700,000 a year to maintain, according to the Australian Treasury’s own modelling. That headline number hides the line items that actually blow budgets, and most of them never appear in a vendor’s quote. This is a CFO’s view of where the money goes, which figures to trust, and why the cheapest-looking engagement is often the most expensive.

Note on terminology: "ASRS" here means the Australian Sustainability Reporting Standards (the AASB S2 climate disclosures), not automated storage and retrieval warehouse systems. If you're a finance or sustainability leader preparing a mandatory climate report, you're in the right place.

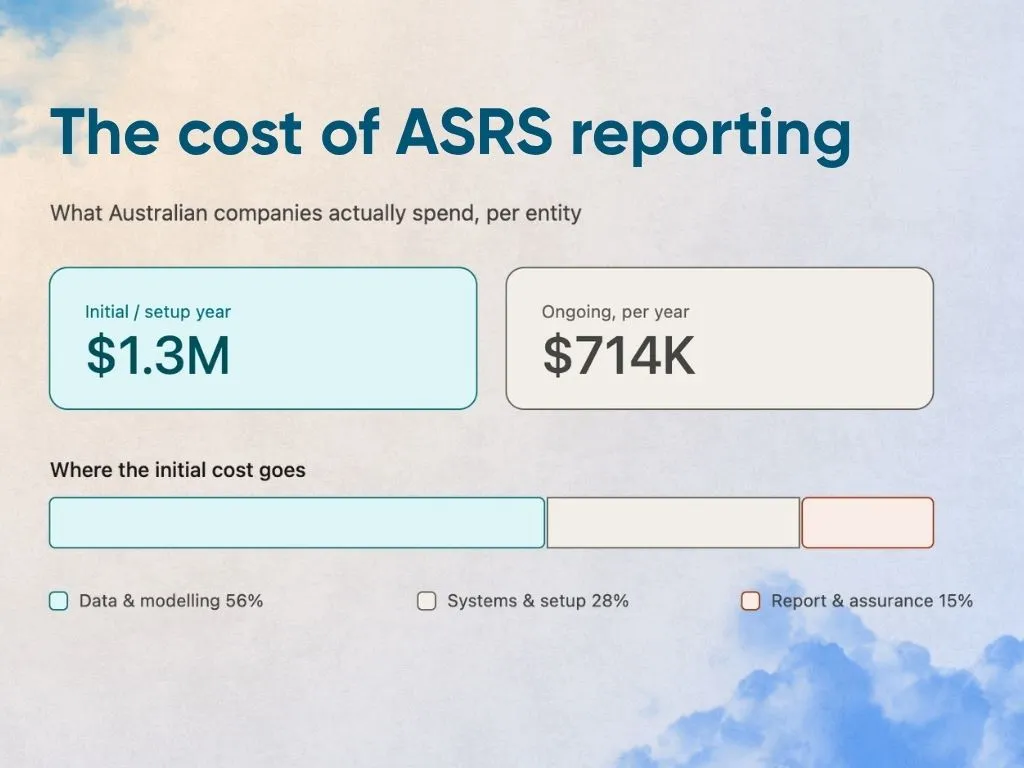

Initial / setup year

$1.3M

Ongoing, per year

$714K

Goes to data & modelling

56%

What ASRS reporting actually costs (the Treasury range, and why it’s misleading)

Almost every article you’ll read quotes the same figure: $1.0 million to $1.3 million per entity, per year. That number comes from the Treasury Policy Impact Analysis: Climate-related financial disclosures (September 2023), the regulatory impact statement that underpinned the legislation. It’s the most authoritative public estimate that exists.

But that “$1.0–1.3M” is specifically Treasury’s estimate of the initial transition cost added to the regulatory burden in the first year, and it’s an average across roughly 1,800 captured entities of very different sizes. Treasury’s own per-firm model is more revealing:

| Cost profile (per entity) | Treasury estimate |

|---|---|

| Initial / transition year | $1,306,847 |

| Ongoing (annual) | $714,032 (reasonable assurance) / $681,154 (limited assurance) |

Source: Treasury, Policy Impact Analysis, Table 7 (Option 1), Sept 2023.

Two things every CFO should take from this:

- Year 1 is front-loaded. Roughly 45% of the first-year cost is one-off: systems, familiarisation, legal review, and the initial build of scenario analysis and Scope 3 models. Budget for a spike, not a flat line.

- The range is about approach, not just size. Treasury costed Australia’s regime above the UK’s TCFD benchmark because AASB S2 is more prescriptive, with mandatory Scope 3 and quantitative scenario analysis. Where you land in the range depends heavily on how much you let software do versus how much you pay people to do by hand.

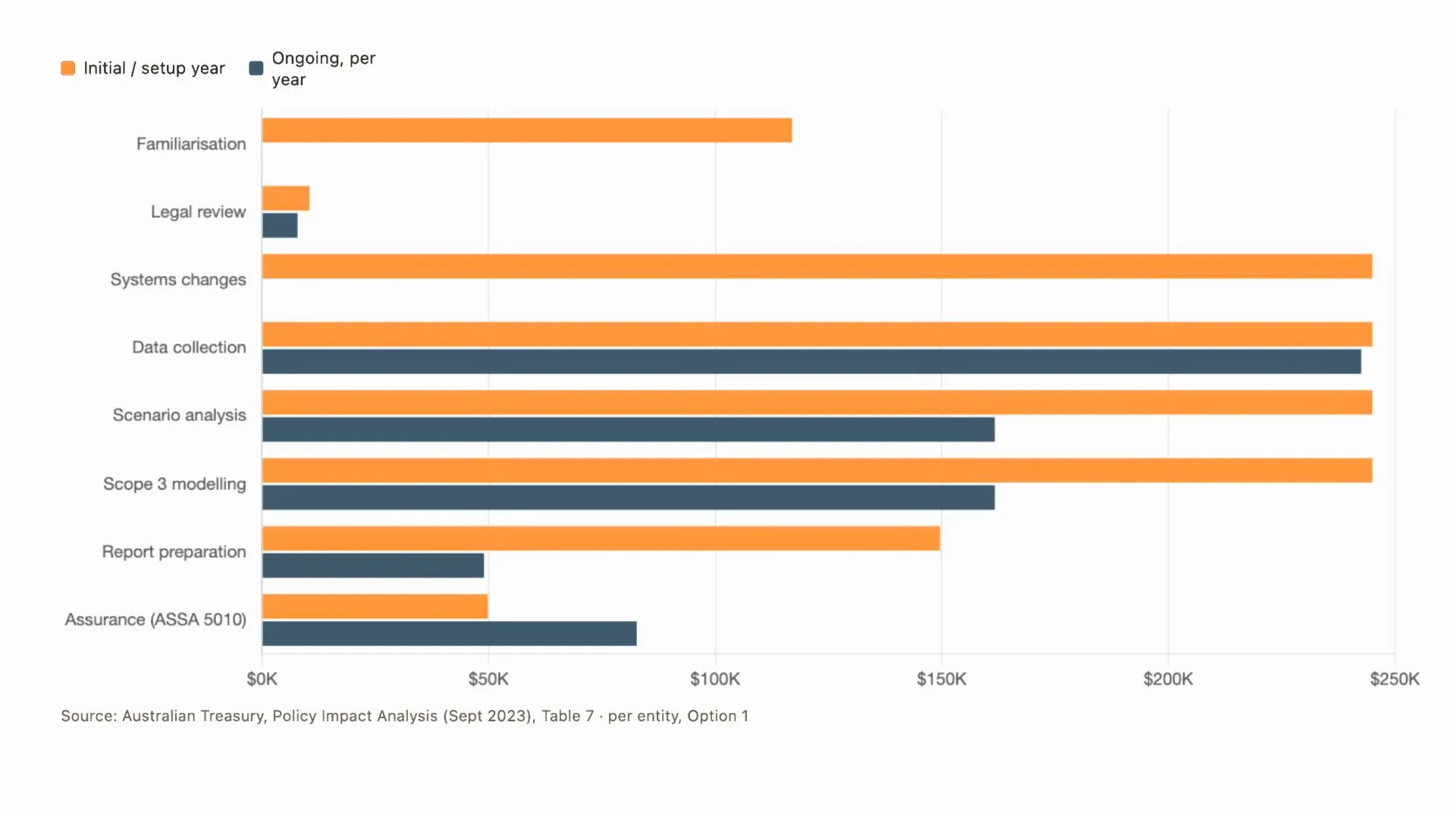

The cost of ASRS reporting, line by line

Here’s the full per-entity breakdown from Treasury’s model. This is the table competitors summarise. We’re showing it in full because the line items are where the decisions get made.

| Cost category | Initial cost | Ongoing (annual) |

|---|---|---|

| Familiarisation & education | $116,960 | — |

| Legal review | $10,472 | $7,854 |

| Systems changes (ICT build) | $245,000 | — |

| Data collection | $245,000 | $242,550 |

| Scenario analysis | $245,000 | $161,700 |

| Scope 3 modelling | $245,000 | $161,700 |

| Preparation of the climate report | $149,600 | $48,960 |

| Assurance (ASSA 5010) | $49,815 | $82,693 |

| Total | $1,306,847 | $714,032 |

Source: Treasury, Policy Impact Analysis, Tables 5–7, Sept 2023. Modelling assumes a blended internal salary of $140,000 uplifted by a 1.75× overhead multiplier (about $245,000 per FTE, about $136/hour).

The single biggest cluster is data and modelling. Data collection, scenario analysis and Scope 3 together account for over half of both the initial and ongoing cost. That is the line a CFO can actually move, and it’s where software pays for itself. The rest — legal, familiarisation and report preparation — is comparatively fixed.

The costs CFOs don’t see coming

Treasury’s model captures the direct cost of preparing a report. In practice, the numbers that surprise finance teams sit in three places the model under-weights.

1. Internal staff time, especially the back-and-forth with the auditor

The Treasury figures assume a defined number of analyst, manager and executive hours to prepare the report. What they don’t fully price is the iterative cycle with your assurance provider once questions start coming back. Under ASSA 5010, the auditor will challenge your emissions boundaries, your estimation methods, your Scope 3 assumptions and your evidence trail. Each query pulls senior finance, sustainability and sometimes legal staff back into the file, often weeks after they thought the work was done.

This is real, recurring, fully-loaded labour cost that lands on people who are already running the business. In my experience it is the most consistently underestimated line in any ASRS budget, and it scales with how messy and manual your underlying data is. Clean, traceable data that a system already holds for you shortens that loop.

2. Assurance (ASSA 5010) is bigger than the quote

Treasury models per-entity assurance at roughly $33,211 to $66,420 for limited assurance on a median ASX300 company, then notes these figures “likely underestimate actual costs.” Two reasons it climbs:

- Assurance scope expands as auditors probe data quality (see point 1).

- The regime steps up over time from limited to reasonable assurance, a higher bar and a higher fee. Treasury’s own ongoing model already prices assurance higher than the initial year ($82,693 versus $49,815) to reflect this.

If you’re budgeting assurance off your first limited-assurance quote, you’re budgeting for the easiest year you’ll ever have.

3. The upfront-breakdown trap

Here’s a pattern I see constantly, and it’s worth a CFO’s attention because it feels like good procurement discipline: companies demand a fixed, itemised price breakdown from a vendor or consultant at the very start, before scope is actually understood.

The problem is that nobody can accurately scope an ASRS engagement before they’ve seen the state of your data, your Scope 3 boundary, and your systems. So one of two things happens:

- The vendor lowballs to win the work, then scope creep drives a series of variations, and the relationship sours over every change order — exactly when you need trust most (during assurance).

- Or the vendor pads the quote heavily to cover the unknowns, and you overpay for risk that never materialises.

The better procurement posture is to price the discovery phase first (a data and readiness assessment), then fix the scope. It costs a little more patience upfront and saves the relationship, and usually the budget, later.

A fixed number you extract too early is the most expensive number in the project. Price the readiness assessment, see the data, then commit to scope — not the other way around.

Cost of ASRS reporting by group and timeline

Your cohort determines both when you report and roughly what you’ll spend. Treasury models three groups plus NGER reporters:

| Group | Entities captured | Indicative cost profile |

|---|---|---|

| Group 1 (largest) | 729 | Full cost (about $1.3M initial); first movers, no market precedent to lean on |

| Group 2 | 755 | About 20% transition discount as methods and data mature across the market |

| Group 3 (smallest captured) | 4,555 | About $45,050 initial / $36,950 ongoing per entity |

| NGER reporters | 362 | About 30% discount; already reporting emissions under NGER and the Safeguard Mechanism |

Source: Treasury, Policy Impact Analysis, Tables 9–11, Sept 2023.

Two planning implications:

- If you’re Group 2 or 3 and not yet reporting, you have a genuine cost advantage if you use it. Methodologies, data conventions and software have matured since Group 1 went first. The mistake is treating “later deadline” as “later start.” The data history you need, especially Scope 3, takes years to build cleanly.

- NGER reporters get a real head start. If you already report under NGER, a large slice of your Scope 1 and 2 data infrastructure carries over to AASB S2 — as long as you’re not maintaining two disconnected data sets. Running one dataset across both frameworks is one of the clearest cost savings available.

If you’re not Group 1: sharing the load without losing control

Most organisations captured by ASRS aren’t Group 1. If you’re Group 2 or 3, you’re likely looking at this cost and thinking the obvious thing: we don’t want to hire a team of full-time people just to produce one report a year. That’s a reasonable instinct, and you don’t have to. But how you share the responsibility matters enormously to both cost and risk.

You can share the work, but you can’t share the governance. AASB S2 prescribes a clear line of governance: the board and management remain accountable for the disclosures, including how climate risk is identified, who oversees it, and how it feeds into strategy. You can bring in external help for the doing, but the ownership has to sit inside the organisation and be documented. Outsourcing the report does not outsource the responsibility.

The trap is fully outsourcing to a consultancy with no technology you own. If a consultant collects your data, builds your models and writes your report but leaves nothing behind that you can maintain, then every time you need to validate a single data point, answer an auditor’s question, or refresh a number next year, you’re back on the phone to an external party, and back on the clock. You’ve rented a report instead of building a capability, and the cost recurs in full every cycle.

My recommendation: use software to handle the repeatable parts, and use external experts for the parts that genuinely need judgement. A platform that lives inside your business handles the recurring, mechanical work — data collection, validation, version history and audit trail — so you’re not paying a consultant by the hour to re-discover your own numbers each year. Then you can use everything a good consultancy does bring: methodology, sector benchmarks, and review.

Where that line should fall, in my experience:

- Most costly to do manually, so lean on tools and specialists: data cleaning without a tool, and scenario analysis, are consistently the most expensive parts of the exercise. Manual data cleaning is bottomless and error-prone, and scenario analysis is technically demanding. These are where software and specialist support earn their keep.

- Can often stay in-house with the right support: governance and strategy — oversight, risk processes and the climate narrative — are areas a capable internal team can own with guidance rather than full outsourcing. This is also the part AASB S2 most expects you to own.

Group 2 has a quiet advantage: the reports already exist. By the time Group 2 reports, Group 1 has already published — a free library of worked examples, including disclosure structures, scenario narratives, and how peers framed governance and materiality. Reading published reports for inspiration is one of the cheapest forms of capability-building available, and it wasn't there for the first movers. Use it before you pay anyone to design from scratch.

How to cut the cost of ASRS reporting without cutting corners

The Treasury model effectively prices the manual path. The categories you can compress are data collection, scenario analysis and Scope 3, because those are driven by repetitive work a tool can do, and they’re more than half the bill.

What actually lowers the number:

- Let software build and maintain the data pipeline so it’s audit-ready by design. The cost isn’t just collecting data, it’s defending it to the auditor. Data that carries its own source, method and audit trail collapses the assurance back-and-forth that quietly inflates every budget.

- Run one dataset across NGER and AASB S2. Stop paying twice to collect the same emissions data for two frameworks.

- Price discovery before you fix scope. Avoid the upfront-breakdown trap; a readiness assessment is the cheapest insurance you’ll buy.

- Combine software with expert support. The most expensive structure is ad-hoc consulting billed by the hour against a scope with no ceiling. A platform plus in-house experts (or accredited partners) covering the whole standard — from data and Scope 3 to scenario analysis, report and assurance support — turns an unpredictable consulting spend into a known cost.

That last point is where NetNada is built to help: audit-ready software plus full-service support that covers all of ASRS, through our in-house team or partner network, so the data is defensible, the scope is clear, and the assurance loop is short. The goal isn’t to do ASRS cheaply. It’s to do it once, properly, at a cost you can forecast.

How software tools should price ASRS work

A good software-led model lets you buy only the support you actually need, and scale it down as your own capability grows, instead of paying full consultancy rates every year. At NetNada we structure this as three options, and the right one depends on how much you want to keep in-house versus hand over:

| Option | Who does the work | What you get | Best for |

|---|---|---|---|

| Do it yourself | Your team, on our platform | AI data ingestion, automatic error flagging, report templates, workflow management and full audit trails | Teams with capacity who want the system to do the heavy lifting and keep cost lowest |

| Do it with you | Your team plus a dedicated expert | Everything in do-it-yourself, plus an account manager and sustainability expert in your corner: emissions boundaries, data-gap resolution, template sharing, and board-review presentations | Teams that can own governance and strategy but want expert backup on the technical calls |

| Do it for you | NetNada, end to end | A fully managed service delivered on our own technology, bringing accumulated knowledge a traditional consultancy can't, plus risk-and-opportunity workshops and in-person training | Teams that want to hand over delivery without losing the maintainable system underneath |

The key difference from a traditional consultancy: even in the do-it-for-you model, the work runs on technology that stays with you. So if you start fully managed in year one and bring more in-house by year three, you’re moving down a path you already own, not starting over. That’s what turns ASRS from a consulting spend with no ceiling into a cost that falls over time.

Working out your own number? Start with our AASB S2 compliance guide to confirm your group and timeline, then walk through how to prepare your first ASRS climate report — or see how audit-ready reporting software compresses the lines that drive the bill.

Sources

- Australian Treasury, Policy Impact Analysis: Climate-related financial disclosures, September 2023 (Tables 5–11)

- AASB S2 Climate-related Disclosures, Australian Accounting Standards Board

- ASSA 5010 Sustainability Assurance Engagements, Auditing and Assurance Standards Board

About the author. Afonso Firmo is a carbon accountant and ASRS consultant at NetNada, where he advises Australian companies on AASB S2 climate reporting, assurance readiness and carbon accounting.

Frequently Asked Questions

Simplify AASB Climate Reporting

NetNada automates AASB-compliant climate disclosures with audit-ready reports. Meet Australian mandatory reporting requirements with confidence.