Basis of Preparation: 2026 Emission Reporting Guide | NetNada

Read time: 9 minutes

I’ve been on a lot of calls with auditors this year. Different firms, different clients, different industries — but the same question keeps coming up in the first 30 minutes:

“Can you send us your Basis of Preparation?”

And the answer, more often than not, is a long pause.

If you’re a Group 1 reporter under ASRS — or you’re going through your first limited assurance cycle — this is the document that gets you in or out of trouble before your auditor has even looked at a single emissions number. So let’s talk about what it actually is, why it matters, and what should be in it.

What is a Basis of Preparation?

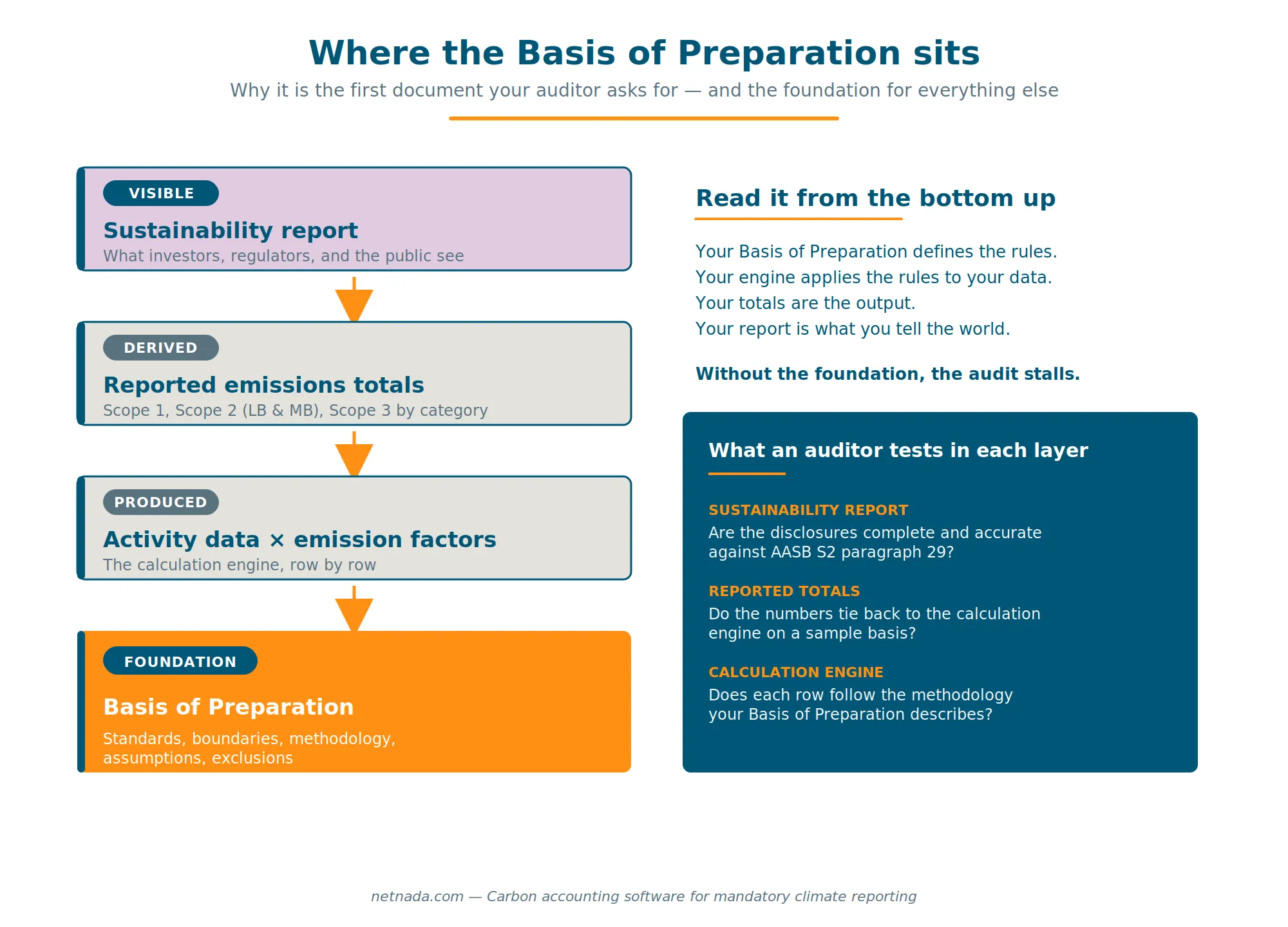

A Basis of Preparation is the document that explains how you produced your emissions numbers — the standards you followed, the boundaries you set, the data sources you used, the assumptions you made, and the things you deliberately excluded.

It is not your sustainability report. It is the methodology document that sits behind your sustainability report. Think of it the way a financial controller thinks of accounting policies: every number in the financial statements rests on a documented policy, and the policy is what the auditor tests against.

For climate disclosure, AASB S2 expects the same thing. Paragraph 29 requires you to disclose your measurement approach, inputs, assumptions, and the source of your emission factors. A Basis of Preparation is how you give your auditor (and your board, and CDP, and anyone else asking) one place to find all of that.

Why it matters more than you think

Three reasons it keeps coming up first in audit kickoff meetings:

It sets the rules of the game. Your auditor needs to know what standards you’re claiming alignment with before they can test against anything. GHG Protocol? AASB S2? NGER? PCAF for financed emissions? If your Basis of Preparation says you follow GHG Protocol Scope 2 dual reporting, your auditor will test for both location-based and market-based figures. If it doesn’t say, they have to ask — and now you’re answering questions instead of providing evidence.

It surfaces the judgements early. Every carbon inventory has judgement calls in it: which consolidation approach you chose, where you drew your operational boundary, when you used spend-based proxies instead of activity data, what you excluded and why. If those judgements are documented up front, they’re defensible. If they only come out under questioning halfway through the audit, they look like rationalisation.

It’s where your “honest disclosures” live. No platform — ours included — does everything the GHG Protocol describes. Maybe you’re not running a quantitative uncertainty model. Maybe your recalculation policy is informal. Maybe you’re using EEIO factors for Scope 3 Category 1 because you don’t have supplier-specific data yet. None of that is a problem if it’s disclosed. All of it is a problem if the auditor finds it themselves.

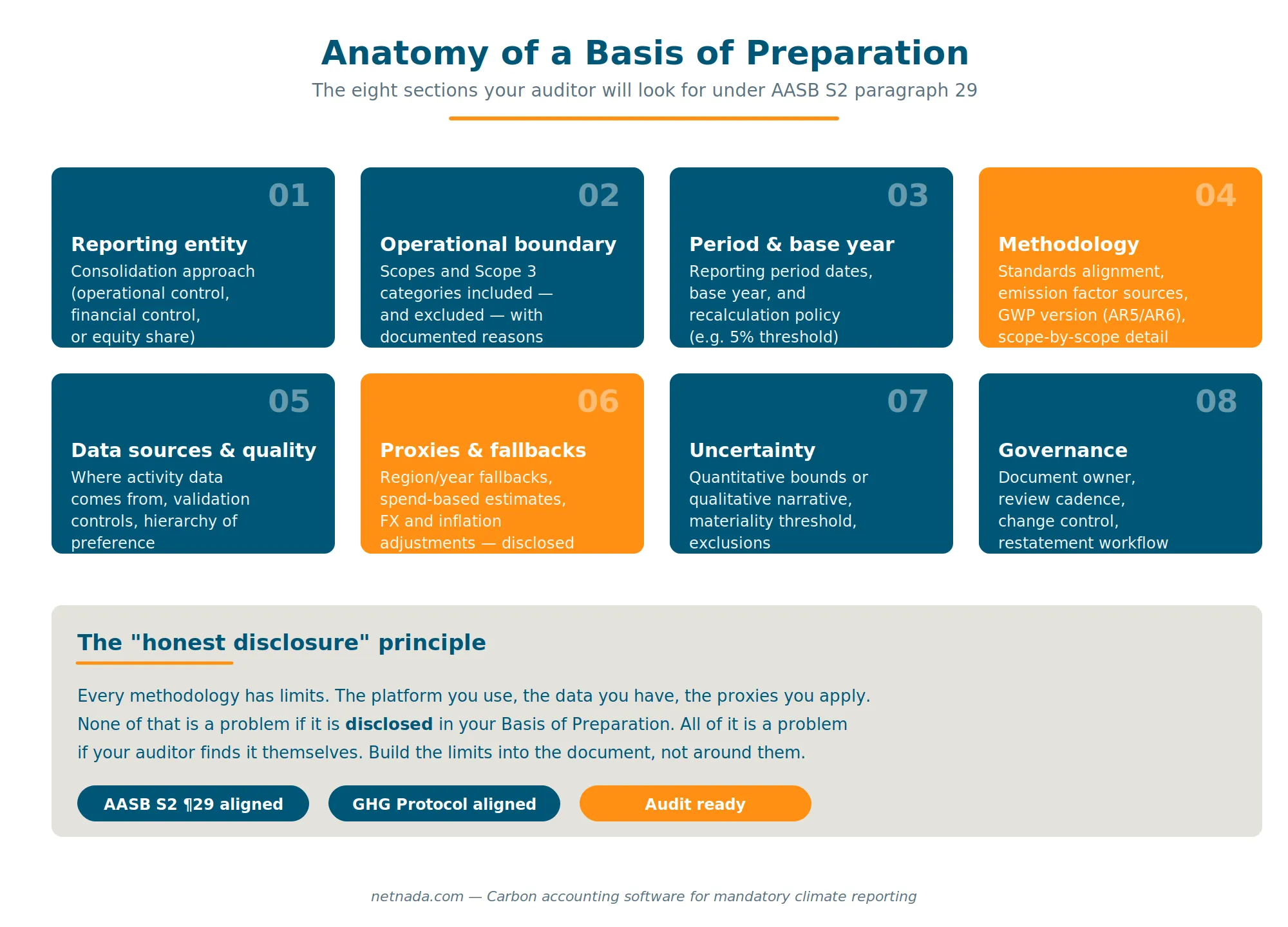

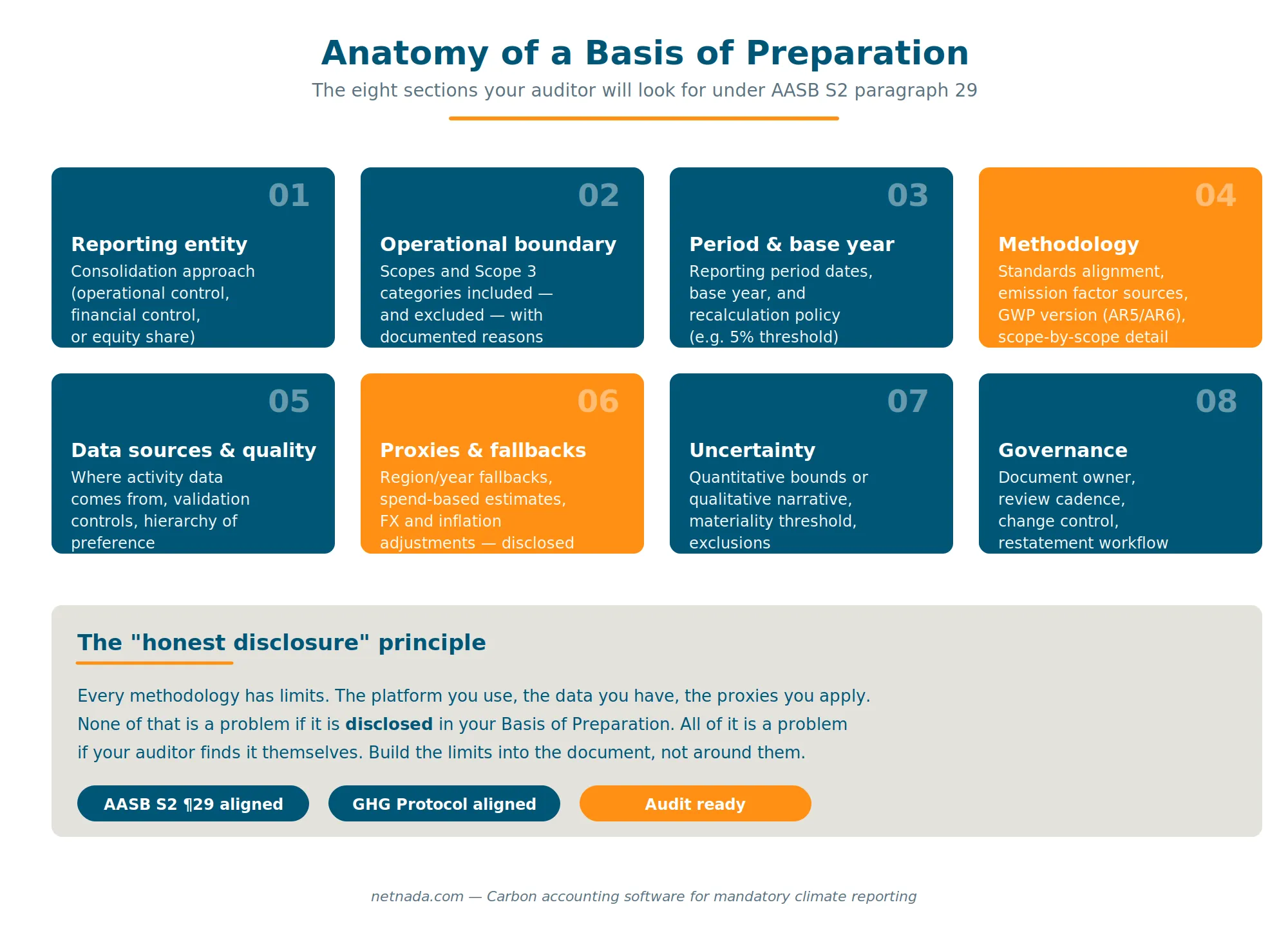

What needs to be in it

A good Basis of Preparation covers, at a minimum:

Reporting entity and boundary. Your consolidation approach (operational control, financial control, or equity share), the legal entities and sites included, and how you’d handle equity-share weighting if that’s what you’ve chosen.

Operational boundary. Which scopes and which Scope 3 categories you include, and which you exclude — with reasons. “Not material” is a fine reason. “We didn’t get to it” is not.

Reporting period and base year. Your reporting period dates, your base year, and your recalculation policy — including the significance threshold (commonly 5%) that triggers a restatement.

Calculation methodology, by scope. The standards you align to (GHG Protocol Corporate Standard, Scope 2 Guidance, Corporate Value Chain Standard, PCAF for financed emissions). The core equation. And, critically, the emission factor sources for each scope, including the GWP assessment report you’re using (AR5 or AR6 — your auditor will ask).

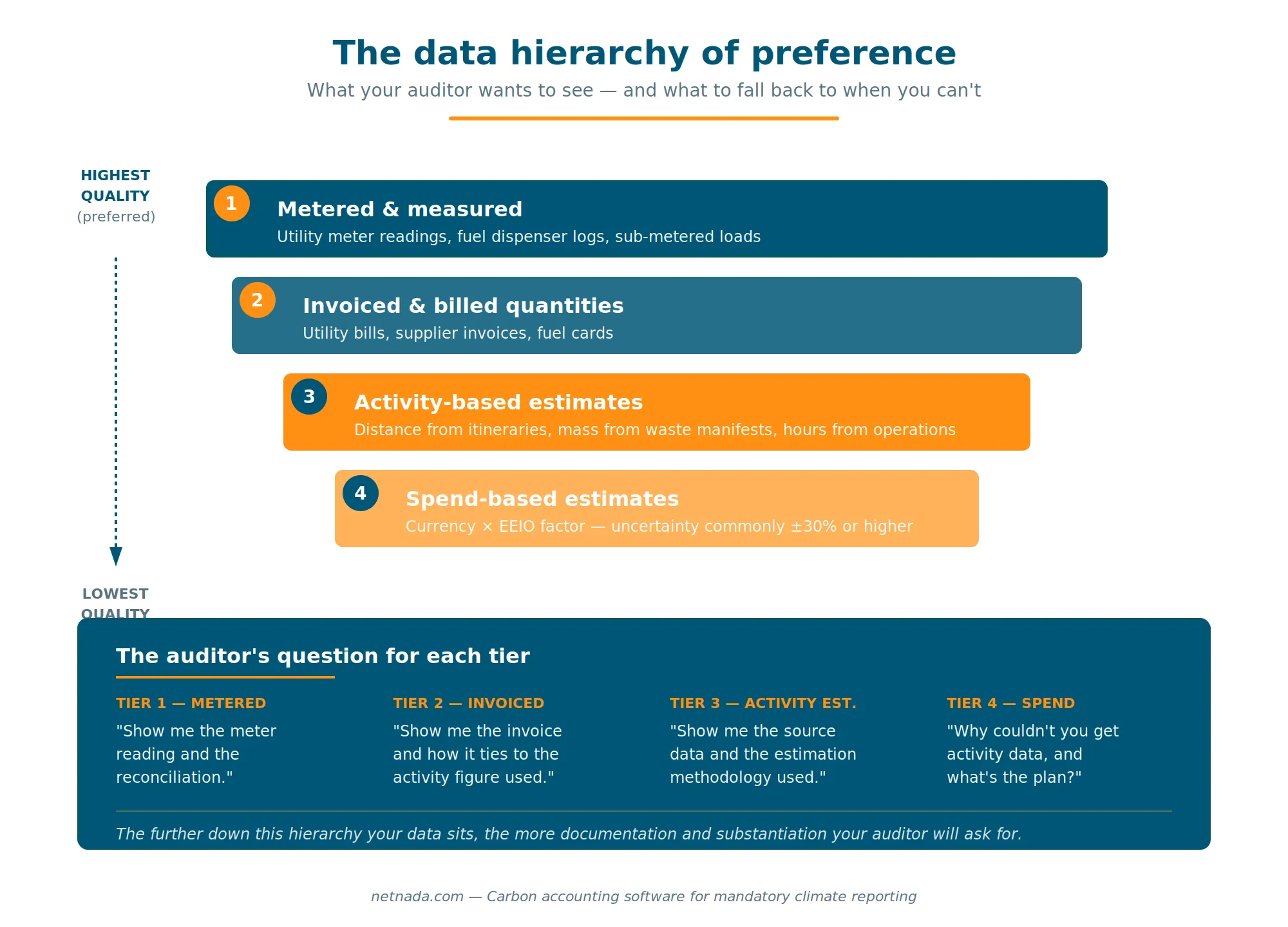

Data sources and quality. Where your activity data comes from, how it’s validated, and your hierarchy of preference: metered data first, invoices second, activity estimates third, spend-based last.

Estimation, proxies, and fallbacks. Every place you used a proxy — a country-level factor when you didn’t have a regional one, an older factor year because the current year wasn’t published, a spend-based estimate because you couldn’t get supplier data — needs to be disclosed and recorded in your audit trail.

Uncertainty and materiality. Whether you produce quantitative uncertainty bounds or qualitative narrative-style disclosure. What materiality threshold (if any) you apply. What you exclude and why.

Governance and change control. Who owns the document, how often it’s reviewed, how methodology changes get versioned, and how prior periods get restated when something material changes.

A real example

We’ve just published the Basis of Preparation that sits behind the NetNada platform — the one we share with our customers’ auditors. It documents exactly the methodology our calculation engine applies: how we select emission factors, how we handle Australian-specific factor coverage (DCCEEW for Scope 1 and 2, Exiobase and CEDA for spend-based Scope 3, AR5 GWP throughout), how dual reporting works under Scope 2 Guidance, how FX and inflation adjustments are applied to spend-based factors, and where the platform’s capability stops short of full GHG Protocol practice so customers know what controls to layer on top.

If you’re working on your own Basis of Preparation — whether you’re using NetNada, another platform, or a spreadsheet — it’s a useful structural template. Steal the section headings, replicate the “honest disclosure” pattern wherever your methodology has limits, and you’ll be most of the way to a document your auditor will actually accept.

Do this week

If you’re in your first ASRS reporting cycle, three things to action this week:

- Find out if you have one. Ask your sustainability lead or your service provider for your Basis of Preparation. If the answer is “we don’t have one,” that’s your priority for next week.

- Pressure-test it against AASB S2 paragraph 29. Walk through the disclosure requirements line by line and check that each one has a corresponding section in your document.

- Get your auditor’s input early. Send them your draft Basis of Preparation before fieldwork starts. The cost of a 30-minute review now is a fraction of the cost of a finding later.

Read the document we use — the same Basis of Preparation we share with our customers' auditors is published as a free, audit-ready template. Use it as a reference, a structural template, or a starting point for your own.

If you want to talk through how to apply it to your own inventory, book a 30-minute walkthrough and we’ll go through it together.

— Afonso

P.S. If your auditor has already asked for your Basis of Preparation and you're still figuring out how to respond, get in touch. We've helped a few Group 1 reporters get this done under deadline pressure this quarter and we're happy to share what worked.

Simplify AASB Climate Reporting

NetNada automates AASB-compliant climate disclosures with audit-ready reports. Meet Australian mandatory reporting requirements with confidence.