Greenhouse Gas Inventory Basis of Preparation

Document the methodology, boundaries, and assumptions behind your corporate GHG inventory in a format auditors, regulators, and assurance providers expect. Free template aligned with the GHG Protocol and ISO 14064-1.

No credit card required. Instant access.

Make Your GHG Inventory Defensible and Audit-Ready

A Basis of Preparation (BoP) is the document that explains how your greenhouse gas inventory was constructed — the organisational and operational boundaries, calculation methodologies, emission factors, data sources, and assumptions applied. Without a BoP, emissions numbers cannot be verified, compared, or trusted. This template gives you a structured, assurance-ready format used by sustainability teams across Australia and globally.

What's Included

Reporting Boundaries

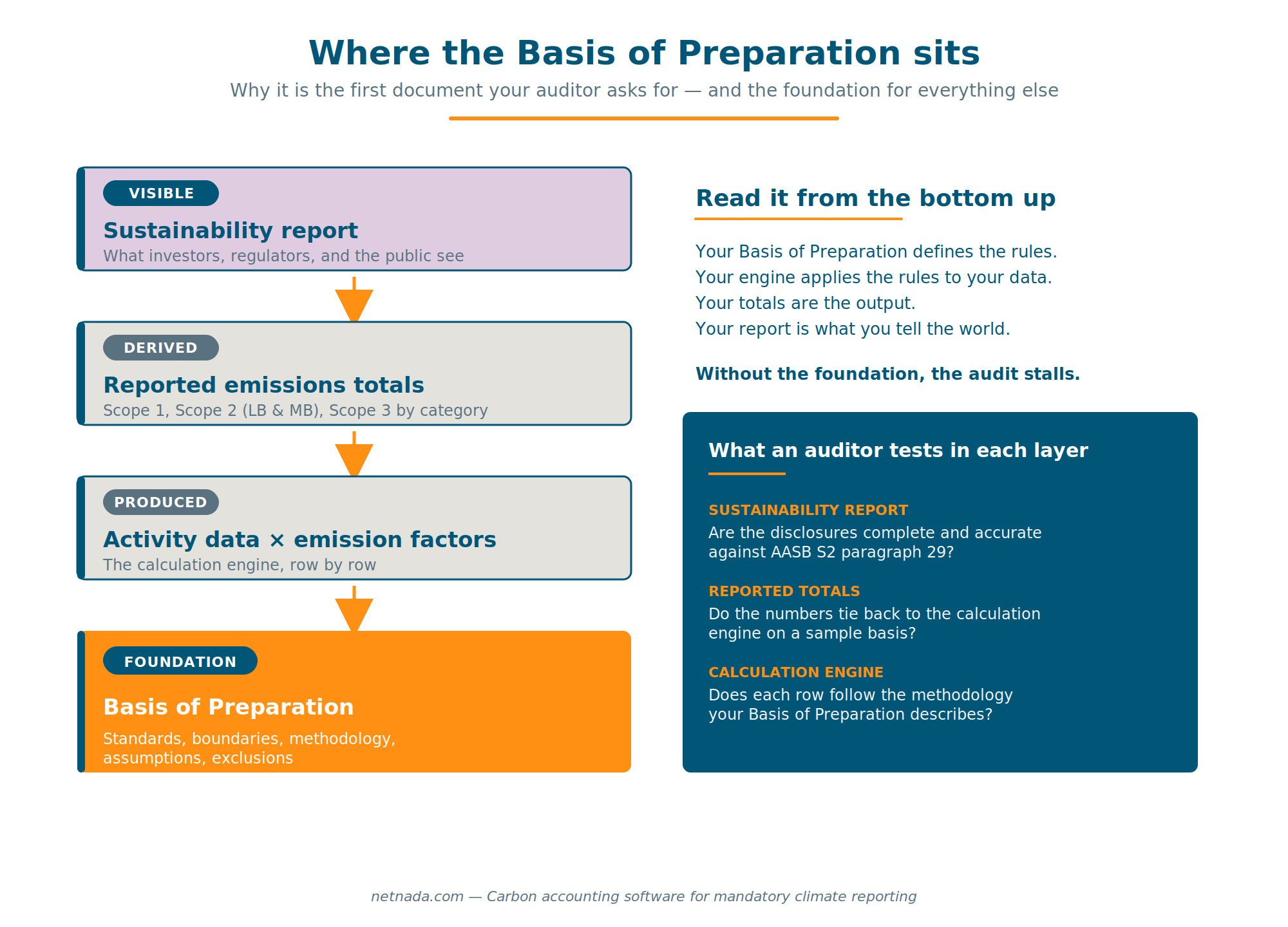

Sections to document organisational boundary (equity share, financial control, or operational control) and operational boundary (Scope 1, 2, and 3 categories included or excluded).

Methodology Documentation

Structured fields to record calculation approach for each emissions source — activity data multiplied by emission factors, with units, conversion factors, and global warming potentials applied.

Emission Factors Register

Template tables to log every emission factor used, including source (NGA, IEA, DEFRA, EPA), publication year, vintage, and the specific scope or category it applies to.

Data Sources and Quality

Sections to record where activity data originates (utility bills, fuel cards, ERP exports, supplier surveys), data quality ratings, and limitations affecting confidence.

Assumptions and Estimations

Documented log for any assumptions, proxies, or extrapolations applied where primary data was poor or unavailable, including rationale and conservatism applied.

Restatement Policy

Built-in framework for documenting your significance threshold and the conditions under which prior-year emissions will be restated (acquisitions, methodology changes, errors).

Why Download This Resource

Pass External Assurance

Auditors require a BoP before issuing limited or reasonable assurance. This template aligns with ISAE 3410 expectations and accelerates the assurance process.

Meet AASB S2 and CSRD Disclosure Requirements

Australian mandatory climate reporting (AASB S2) and EU CSRD both require disclosure of methodology and assumptions. The template covers required disclosures.

Year-on-Year Consistency

Locks in methodology decisions so emissions are calculated consistently across years, enabling credible trend reporting and target tracking.

Defensible CDP and Science Based Targets Submissions

CDP scoring rewards methodology transparency. Science Based Targets initiative (SBTi) validation requires documented inventory boundaries and approaches.

Perfect For

Download the Free Basis of Preparation Template

Get the audit-ready template used by sustainability teams to document their GHG inventory methodology. Aligned with the GHG Protocol, ISO 14064-1, AASB S2, and CSRD requirements.

🔒 Your information is secure. We'll never share your details.

What a Basis of Preparation Does

A Greenhouse Gas Inventory Basis of Preparation (BoP) is the methodological foundation of every credible carbon report. It captures, in one controlled document, every choice made during inventory construction — what was included, what was excluded, how each number was calculated, and what limitations apply.

Without a BoP, an emissions figure is just a number. With a BoP, it becomes a defensible, repeatable, and auditable disclosure that withstands scrutiny from regulators, assurance providers, investors, and customers running supply-chain due diligence.

Why It Matters Now

Australian climate-related financial disclosure under AASB S2 has moved from voluntary to mandatory for large entities, with smaller groups phasing in through the late 2020s. Disclosure of methodology and significant assumptions is explicitly required. The EU’s CSRD and the ESRS E1 standard have equivalent requirements for European operations and supply chains.

Beyond regulation, voluntary frameworks have raised the bar:

- CDP scoring criteria explicitly reward methodology transparency and consistency.

- Science Based Targets initiative (SBTi) validation requires documented inventory boundaries and Scope 3 screening.

- External assurance providers under ISAE 3410 cannot issue an opinion without a BoP to test methodology against.

What the Template Covers

1. Reporting Period and Reporting Entity

Defines the entity name, reporting period (typically a financial year), and the legal and operational structures included.

2. Organisational Boundary

Documents the consolidation approach selected — equity share, financial control, or operational control — and the rationale for the choice. Lists all entities included and any joint ventures, associates, or franchises with their consolidation treatment.

3. Operational Boundary

Records which emissions are included by scope:

- Scope 1 — direct emissions from owned or controlled sources (stationary combustion, mobile combustion, fugitive emissions, process emissions).

- Scope 2 — indirect emissions from purchased electricity, steam, heating, and cooling. Includes both location-based and market-based methods.

- Scope 3 — value chain emissions across the 15 GHG Protocol categories. Documents which categories are included, which are screened out, and the materiality reasoning.

4. Calculation Methodology

For each emissions source, the template records:

- Activity data type and unit (kWh, litres, tonne-km, AUD spend)

- Emission factor source, vintage, and units

- Global warming potentials applied (typically AR5 or AR6 100-year)

- Calculation formula and any conversions

5. Emission Factors Register

A consolidated table listing every factor used, its source publication, year, and applicable scope. Common sources include the Australian National Greenhouse Accounts (NGA) Factors, IEA, DEFRA/BEIS, US EPA, ecoinvent, and EXIOBASE.

6. Data Sources and Quality

Captures where activity data originates (utility invoices, fuel card statements, expense systems, supplier surveys, modelled estimates) and assigns a data quality rating to each source. Highlights gaps and the impact on inventory confidence.

7. Assumptions and Estimations

A log of every assumption, proxy, or extrapolation applied — for example, prorating partial-year occupancy, using industry averages where supplier-specific data is unavailable, or assuming default work-from-home patterns. Each entry records the rationale and any conservatism built in.

8. Exclusions

Lists emissions sources or Scope 3 categories that are excluded, with the materiality justification. The GHG Protocol allows exclusions where emissions are not material, but they must be disclosed.

9. Restatement Policy

Defines the significance threshold (commonly 5% of total emissions or scope-level emissions) above which prior-year emissions will be restated. Documents the conditions triggering restatement — acquisitions and divestments, methodology changes, emission factor updates, error corrections.

10. Governance and Sign-Off

Records preparer, reviewer, and approver for each inventory cycle, the date of approval, and the version history.

How to Use the Template

- Read through the structure — the template is sectioned to map directly to disclosure requirements under AASB S2, CSRD, and ISO 14064-1.

- Populate during inventory build — document decisions as you make them, not retroactively. Retroactive documentation is the most common audit finding.

- Have it reviewed before assurance — share the BoP with your assurance provider before fieldwork. Most assurance friction comes from methodology ambiguity, not data errors.

- Update annually — review with each inventory cycle. Archive previous versions so the audit trail is preserved.

- Reference it in your sustainability report — the public report should state that emissions are prepared in accordance with the BoP, which is available on request or annexed.

Frameworks the Template Aligns With

- GHG Protocol Corporate Accounting and Reporting Standard (Scope 1 and 2)

- GHG Protocol Corporate Value Chain Standard (Scope 3)

- ISO 14064-1:2018 — Specification with guidance for the quantification and reporting of GHG emissions

- AASB S2 / IFRS S2 — Climate-related Disclosures

- ESRS E1 — European Sustainability Reporting Standard, Climate Change

- CDP Climate Change Questionnaire — methodology disclosure questions

Common Pitfalls This Template Helps You Avoid

Pitfall: Inconsistent emission factors across years How the template helps: The Emission Factors Register requires source and vintage to be logged, making changes visible and triggering documented restatement decisions.

Pitfall: Undocumented Scope 3 exclusions How the template helps: The Exclusions section forces explicit disclosure of which of the 15 categories are out of scope and why.

Pitfall: Mismatched organisational boundary between financial accounts and emissions inventory How the template helps: The Reporting Entity and Organisational Boundary sections require explicit alignment with the financial reporting entity, satisfying AASB S2’s connected information requirement.

Pitfall: No restatement policy, leading to ad hoc decisions when prior years are republished How the template helps: A pre-defined significance threshold and trigger list removes year-end ambiguity.

Pitfall: Methodology decisions stored across emails and spreadsheets, lost when staff change How the template helps: A single controlled document with version history preserves institutional knowledge.

Next Steps

- Download the template and review the sections against your current documentation.

- Identify gaps — most companies preparing their first BoP discover that emission factor sources, assumptions, and exclusions have never been documented in one place.

- Populate during your next inventory cycle rather than retroactively. Document decisions as they are made.

- Engage your assurance provider early — share a draft BoP before fieldwork to flag any methodology concerns before they become audit findings.

- Establish a review cadence — annual review, with version control, ensures the document stays current as your business and regulatory environment evolve.

Frequently Asked Questions

A Basis of Preparation (BoP) is a formal document that describes how a company's greenhouse gas inventory was prepared. It explains organisational and operational boundaries, calculation methodologies, emission factors, data sources, assumptions, and limitations. It is the methodological backbone that allows emissions data to be independently verified, compared across years, and trusted by regulators, investors, and assurance providers.

Under Australia's mandatory climate-related financial disclosure regime (AASB S2), entities must disclose the methods and assumptions used in measuring Scope 1, 2, and 3 emissions. The EU's CSRD and ESRS E1 contain equivalent requirements. While the document is not always called a 'Basis of Preparation' in regulation, the disclosure substance is mandated. For voluntary frameworks like CDP and SBTi, a BoP is effectively required to score well or achieve validation.

A sustainability report communicates results to stakeholders. A Basis of Preparation explains how those results were calculated. The BoP is typically an internal control document referenced in the sustainability report or annexed to it, ensuring numbers in the headline report are traceable, repeatable, and auditable.

Best practice is approval by the Head of Sustainability or equivalent, with sign-off from Finance (for the carbon-financial linkage required under AASB S2 and IFRS S2) and review by Internal Audit or Risk if the function exists. The BoP should also be shared with external assurance providers before fieldwork begins.

Review annually as part of the inventory cycle. Update whenever there are material methodology changes, acquisitions or divestments altering organisational boundary, new emission factor releases, or category additions (e.g., expanding Scope 3 coverage). Each version should be dated and earlier versions archived.